Homebuilders: Investment Thesis

I put the cart before the house in my last post...

I put the cart before the horse in my last post.

I realized before I profile select publicly traded homebuilders, I first need to explain the broad long-term investment thesis for them.

As I previously (link) laid out, there is a labor shortage in construction - which may become even worse.

And I see this benefiting big builders. We have multiple other beneficial factors as well helping out big builders which we'll get to in a bit…

This may sound counter intuitive. Why would less construction workers benefit them?

Because I see them attracting more of the available workers. And pulling workers away from smaller contractors enabling them to grow revenues and take a bigger piece of market share - public builders make up about 53% of new homes built. There is plenty of market share for the taking.

Bigger builders can be in a better financial position giving them more financial flexibility than smaller builders.

And this position and flexibility comes from several sources.

A few examples are:

Having economies of scale.

The ability to receive better financing terms.

Seizing opportunities smaller companies can't.

Building their own large developments.

(I know I'm glossing over these. However, individual factors will get unpacked for each company profiled.)

For now, we can trust the word of Jeffrey Mezger the CEO of KB Homes, one of America's largest homebuilders. In a recent interview he touched on several of these examples saying:

“We're taking [market] share from two sources. One is smaller builders that are having difficulty with financing. Banks are very conservative right now on what they'll lend a small builder to go develop lots.”

The other source Mezger mentions in favor of big builders taking market share is the lack of existing homes for sale. Another topic we'll get to shortly…

And the above examples along with growing market share enables these companies to do another thing that smaller builders may struggle with - attract more workers.

Bigger builders can offer job security, higher pay, and benefits. Employee benefits alone are big. It's one that can be absent in the construction industry.

This is because more work is contracted out. Especially when it comes to smaller contractors.

Insurance is an expensive overhead cost in the construction industry. Workmen's compensation is around 1% - 2% of paid wages, assuming no incidents.

And then there are federal and state unemployment taxes.

Construction projects are generally put to bid. Cutting any employer costs by shifting the burden lowers overall project costs, increasing the odds of winning bids.

So, if we see a crew of workers there's a decent chance all or most of them aren't receiving w-2 wages. They receive a 1099, or are self-employed, workers - even if the arrangement is more like an employer/employee.

The National Association of Homebuilders (NAHB) found over 23% of workers in construction are self-employed. This is compared to just 10% of the broader workforce.

And I see big builders getting a larger boost in workers if undocumented workers start leaving the industry.

There are about 2.1 million undocumented workers in the construction industry. This is around 15% of the workforce.

An exodus of even a portion of these workers will hinder the ability for construction companies to find laborers.

And for the remaining workers they have greater bargaining power since their skillset is in greater demand.

Meaning they'll likely go where they get compensated the most - bigger construction companies.

If I were in the trades, I'd opt for a larger company. That way I'd feel more secure in providing for my family.

I know a lot of spilled words over labor. However, we can't automate homebuilding.

Without workers homes can't be built.

This gives larger builders with bigger workforces a leg up to meet the demand for more housing.

Now onto our other beneficial factors working to homebuilders' advantages.

I see six big themes working as tailwinds for homebuilders. And I'll cover each of these in order as their own section:

Demand

Affordability

Lower interest rates

Regional Strength

Build-to-Rent communities

Generally solid economy

Now let's get to our big themes.

Demand, lots of Demand

America is short roughly 4.7 million homes.

If we missed my last post, I went into detail about this shortage. And how we got to this deficit. To save the ink, and not be redundant, I'll not repeat too much of myself here.

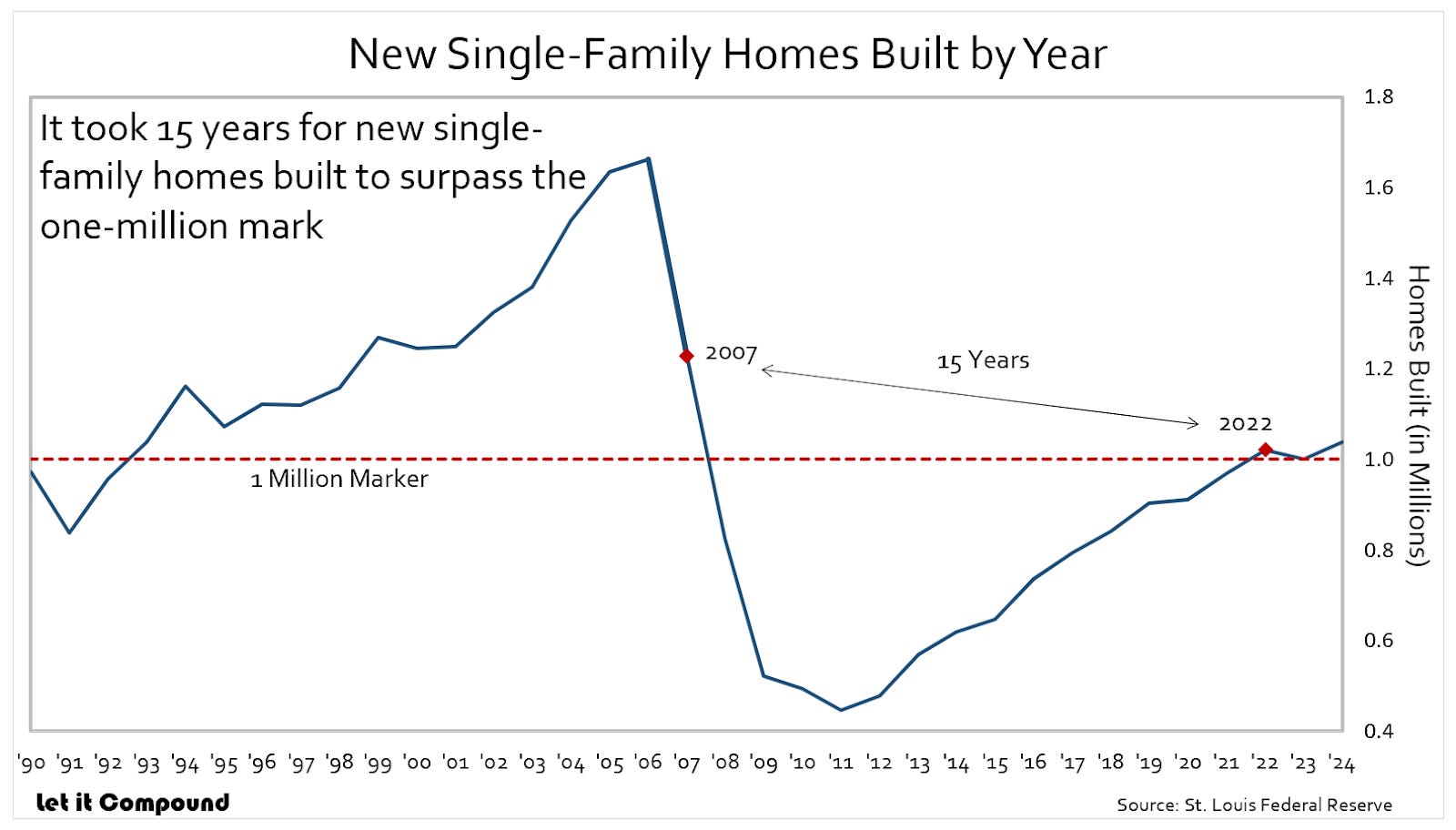

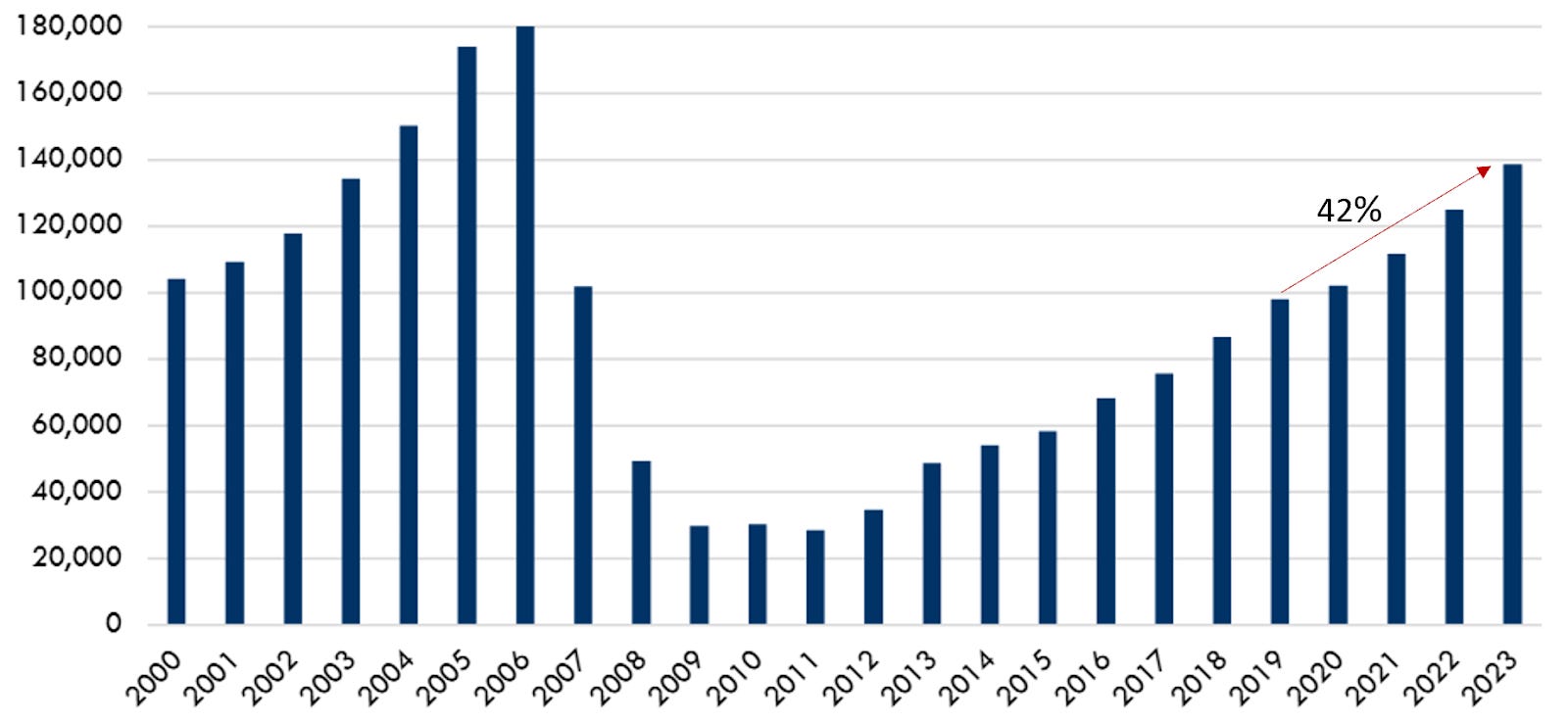

This shortage is despite new homes being constructed at a rate that's at multi-decade highs.

During both 2022 and 2023 new homes built surpassed the one million marker. This was the first time this occurred since 2007, during the housing bubble run up.

We can see how many new single-family homes were built per year in the chart below.

This is great for homebuilders. They are producing homes at levels not seen since the housing boom. And while doing so having a multi-year runway to fill the deficit of nearly five million homes.

What's more is it's likely this deficit will continue persisting because of two major generational cohorts - Millennials and Gen Z.

There are 73 million millennials in America. This cohort is currently in the age range of 28 to 43 years old. They are in the midst of their prime years for spending and home buying.

The real estate data and analytics company, CoreLogic, sees “millennial home buying demand is likely to remain strong over the coming years.”

This is likely because 55% of millennials own a home, leaving 45%, or 33 million people, who may still be seeking to buy.

Then we also have Gen Z. There are another 70 million people in this generation. And they are just coming of age for homeownership. The oldest of Gen Z is now 27 years old, entering prime spending years.

While the youngest is still just 12 years old…

I'd expect the homeownership percentage of each of these generations to match Baby Boomers - 80% of Baby Boomers own a home.

So that means, tens of millions of homes need to swap hands or be built…

And homebuilders don't only have demand trends in their favor - new homes make financial sense.

Which is our next theme, affordability.

New for the Price of Used

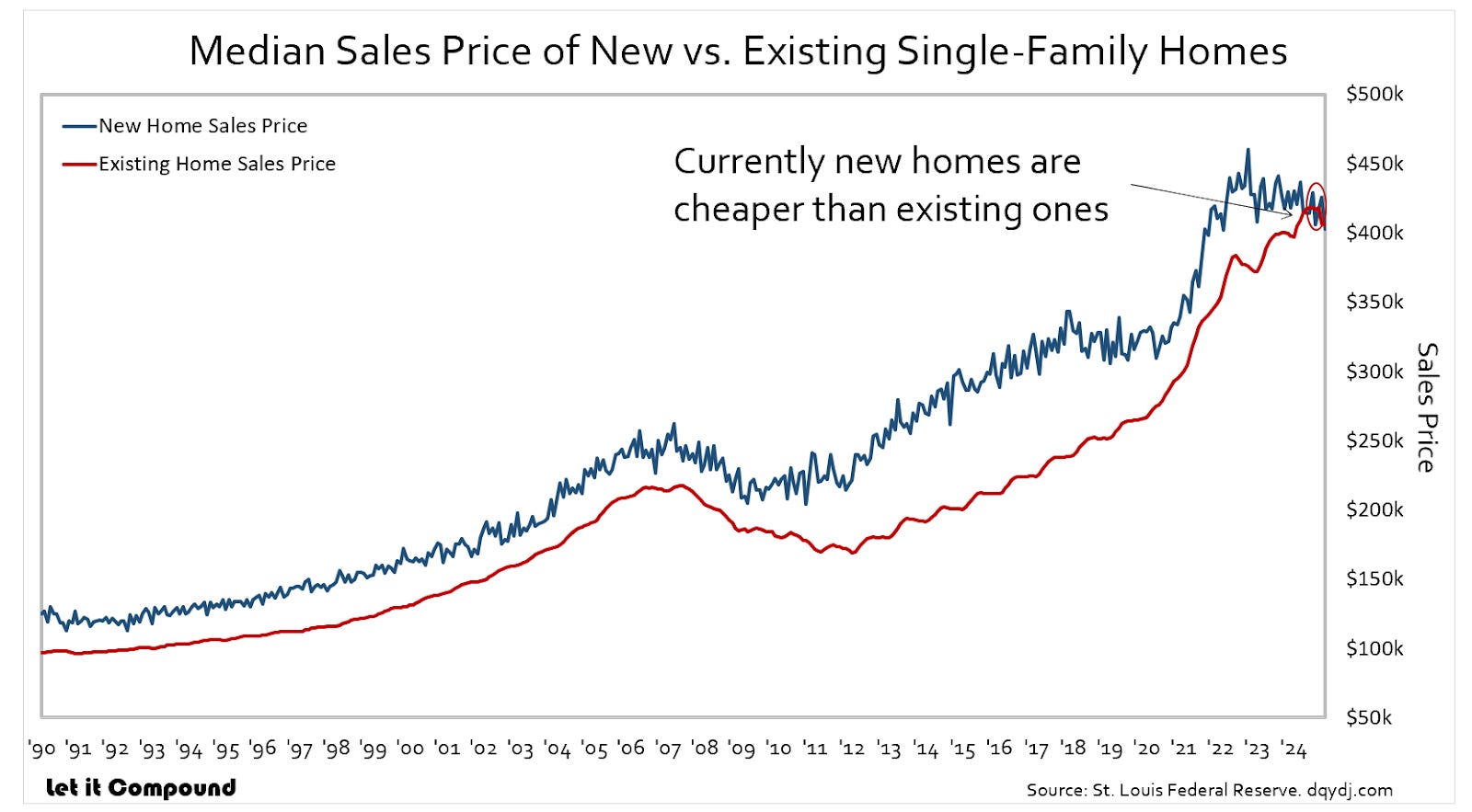

Historically new homes came at a premium compared to buying an existing home. However, this gap has closed.

And to me, this is great for builders. You get a new home for the price of used, that's a deal.

Prior years there was a meaningful premium for new homes. Buying an existing home, one could save big on their down payment while having lower mortgage payments.

However, that's not so much the case now.

Currently the median price of a new home is $402,600. That's actually $3,500 less than the median price for the sale of an existing home which is $406,100.

This is crazy. And historically unprecedented.

We can see in the chart below in previous years there was much more price disparity.

What's more is new buyers won't have the cash outlay of updates and repairs.

They'll get a new home, one that's very likely much more energy efficient and has lower maintenance cost, for the price of used.

Where I live existing homes are selling for over $465k. And you'll likely be buying a house that hasn't been updated for decades.

I'm talking not only about cosmetics but it's common that house systems, roofing, windows, and other big-ticket items are at or near the end of their lives.

The trend is to let the next person deal with it because there is no other option. Not enough homes are available.

Maybe it’s anecdotal. However, when I search around the U.S. for homes it seems fairly par the course. It makes financial sense in these cases to buy new.

And that's good for home builders - as is our next theme, interest rates.

Interest Rates - Lower, Just Slower

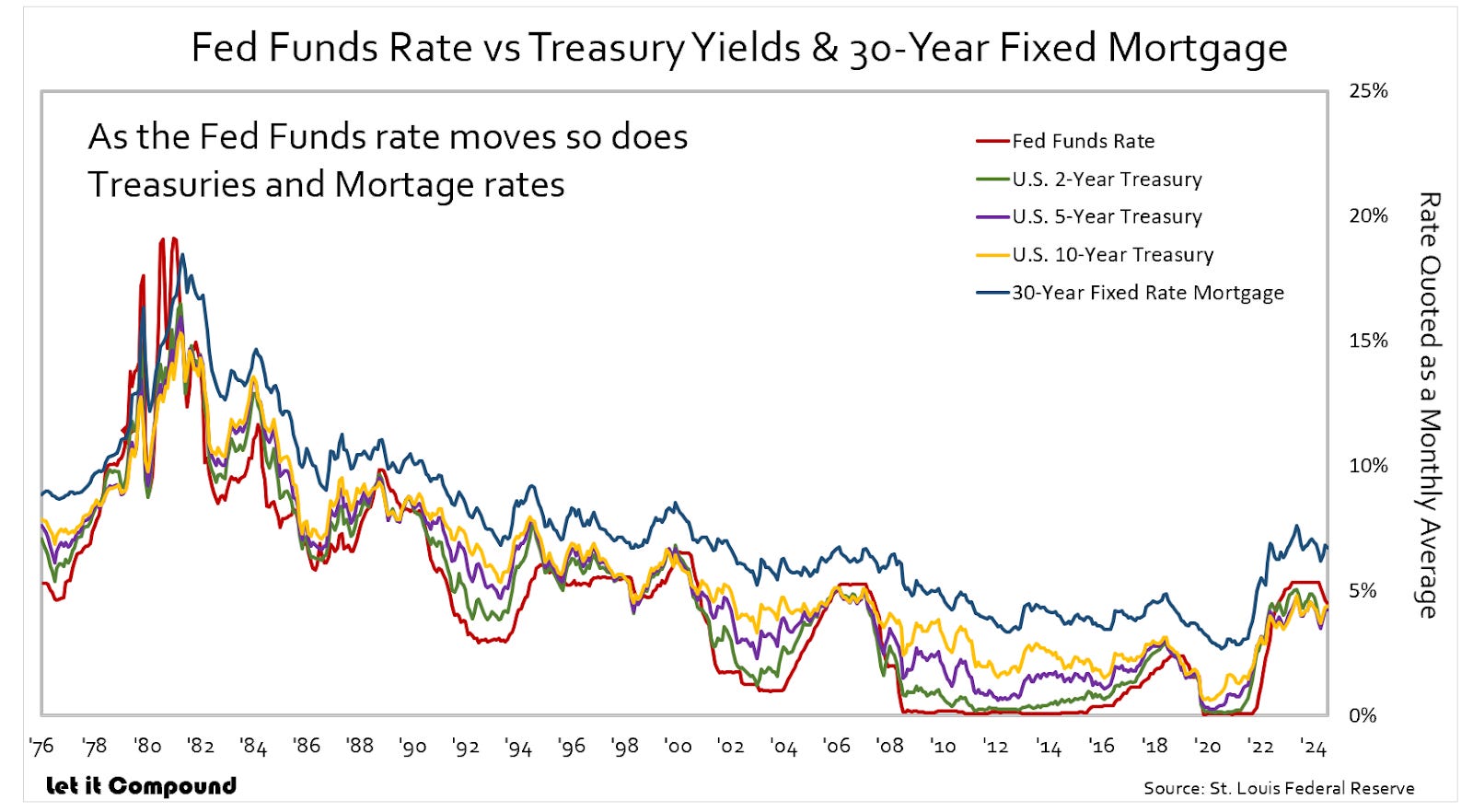

Since September the Fed Funds rate is down 100 basis points, or one full percentage point. This rate is set by the Federal Reserve. And is the rate banks charge one another for overnight lending.

Why is this important? It's the baseline for interest rates.

Below we can see how the varying yields of treasury durations and the 30-year mortgage rate reacted since the Fed started its historic rate hike in March 2022.

We may notice that even with the lower Fed Funds rate yields haven't really fallen in line.

This is because investors weren't and aren't getting ahead of themselves on rate cuts. And currently strong economic and inflationary data could give grounds for keeping rates steady - through 2025.

However, we are starting to see mortgage rates trending lower. As I write the 30-year mortgage rate is 6.9%, down from its peak of 7.4% in late 2023.

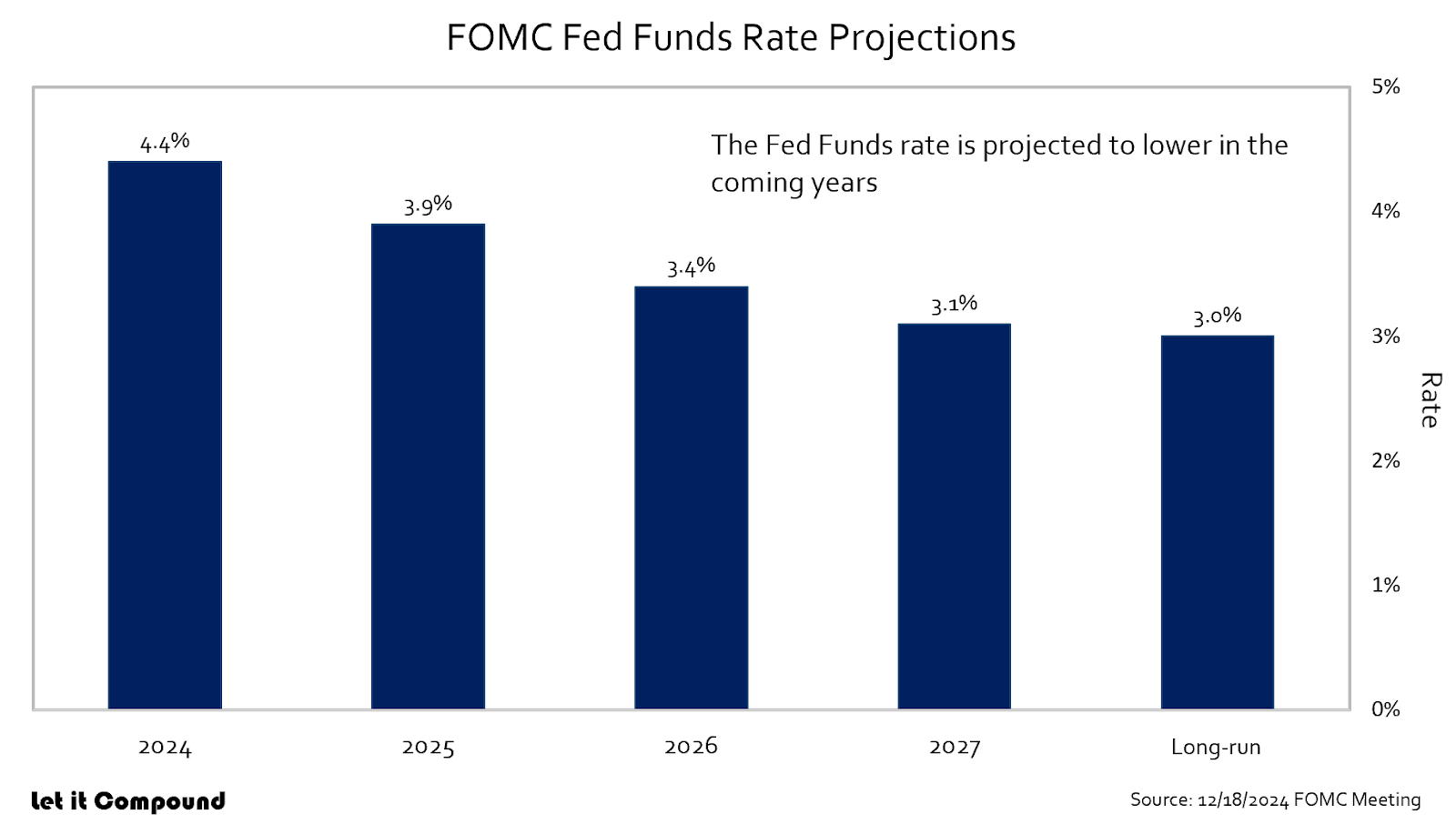

And the Federal Reserve is targeting a Fed Funds rate of 3.1% in 2027.

We can see this in the projections from the Federal Open Market Committee (FOMC). This committee consists of 12 members made up of Federal Reserve

System Governors and Bank Presidents. These are the people who sway Monetary policy.

Meaning it's likely mortgage rates will dip to around 6%. On average the 30-year mortgage is roughly equal to Fed Funds Rate + Three Hundred Basis Points (3%.)

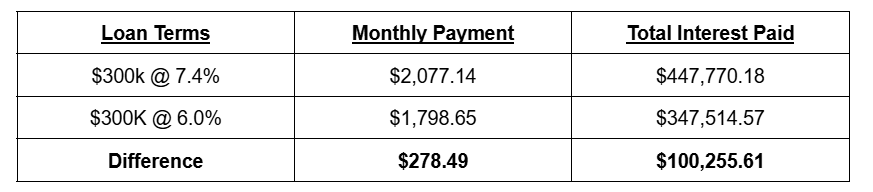

6% versus 7.4% makes a big difference when it comes to monthly mortgage payments. And to the total amount of interest paid over the life of the loan.

Here is a look at a $300k loan comparing the two rates and the impact they have.

These are big savings in a seemingly small move in absolute terms of percentage points.

And at the 6.0% level for the 30-year mortgages, compared to the current 6.9%, studies from the NAHB find that home ownership will become attainable, by becoming affordable, for roughly 4.5 million more households.

In addition to lower rates, big builders can make financing cheaper for buyers.

When we bought our house, I ran the numbers, and it made sense to buy down points. This is where borrowers can pay a lump sum of cash to lower the interest rate on their mortgage or “buy down points.” By doing so we lower monthly mortgage payments.

However, this one-time expense is spendy, costing a couple grand.

What big builders can do is take on this cost to incentivize buyers.

In turn it enables them to move their inventory. Then they can redeploy the capital in building more homes.

Whereas a smaller builder or speculative investor likely couldn't eat the costs.

This also plays into affordability as buyers have more manageable monthly payments. I decided to have it in this section as it relates to interest rates.

Next theme. Regional population and housing demand growth.

Big Markets are Getting Bigger

Here, my goal is to show where the major markets are. And what areas people are moving to.

Why people are moving to these places is out of the scope of this thesis - just knowing people are moving and settling roots is what's important.

And I'll be going into greater detail for specific builders in their respective profiles.

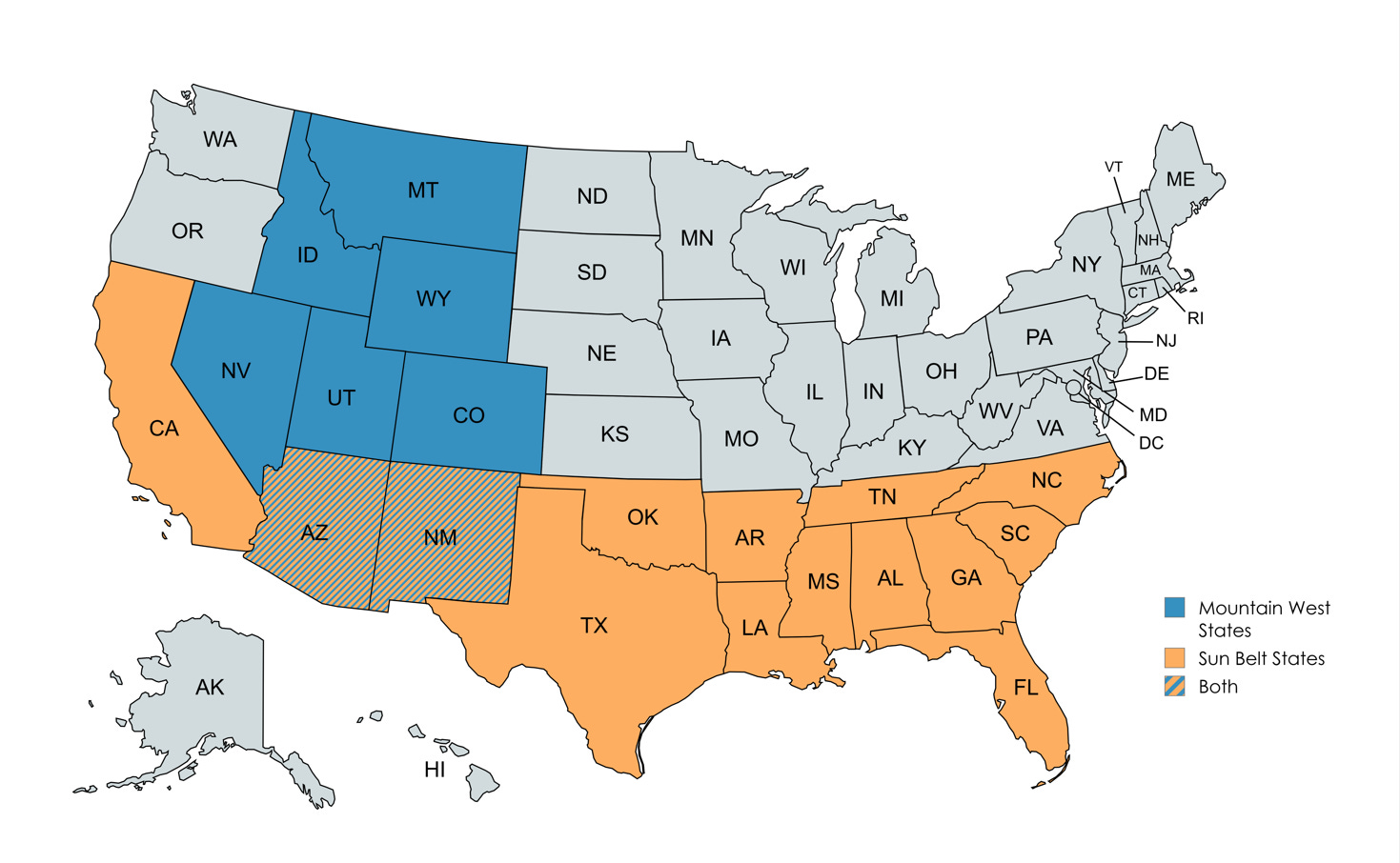

The two key regions I'll highlight here are states in the Sun Belt and the Mountain West.

The Sun Belt states are the 15 states in the southern half of the United States.

While the Mountain West are the eight states that the Rocky Mountains run through.

I have the states color coded below.

Created using mapcharts.net

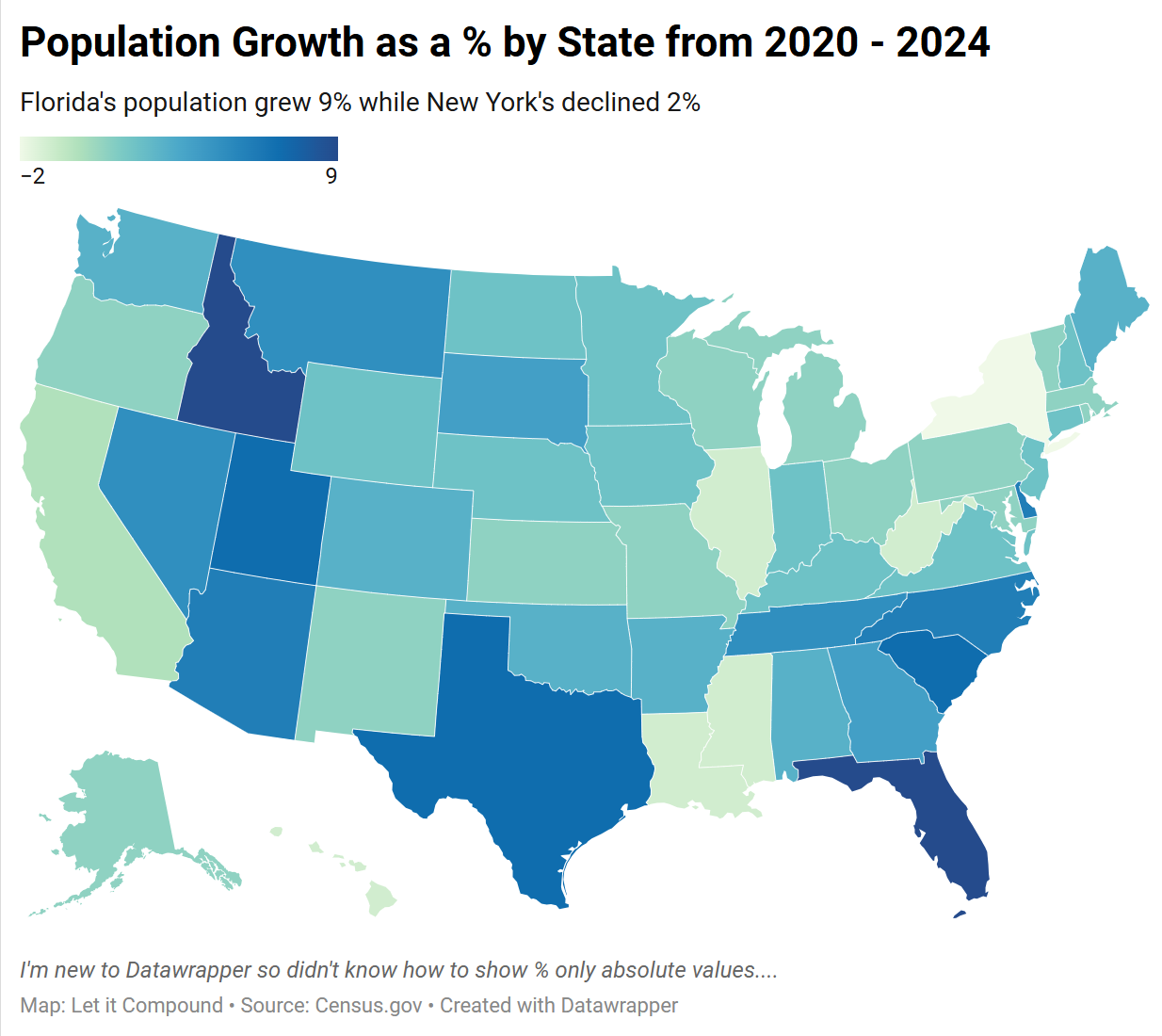

And the following graphic shows the states within these regions have growing populations.

(If we want to interact with the chart we can with this link)

We'll notice since 2020 Florida’s population has increased 9% while Texas grew 7%.

These states have large growing metros attracting more people to live there. And driving housing demand.

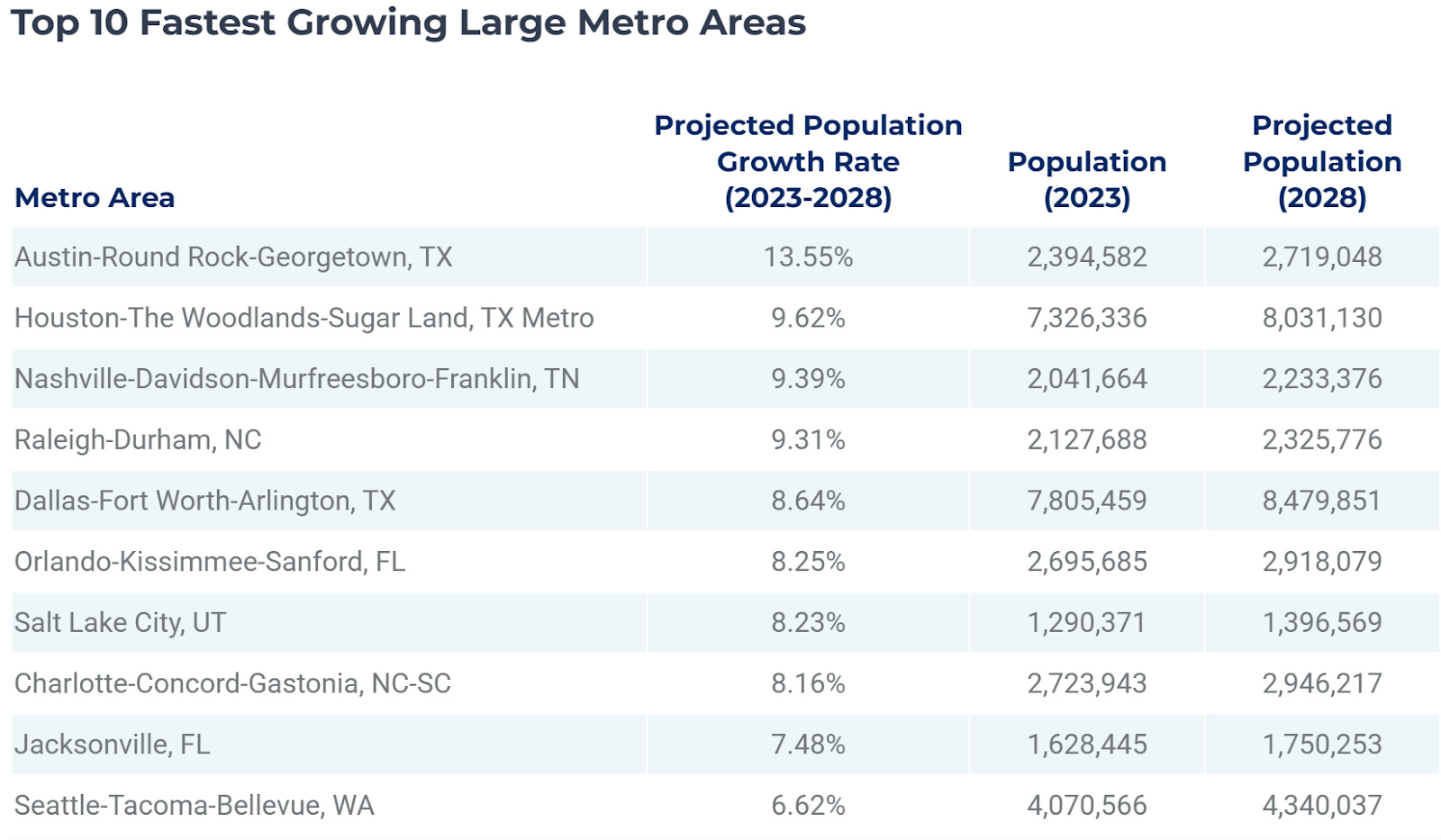

We can see in the following table showing the population and expected growth of the top 10 fastest growing large housing metros in the U.S.

Source: Site Selection Group

Unless something unforeseen alters these cities, or other cities grow and become more appealing, these metros will continue to grow.

Even if a new metro starts gaining traction, the big builders will grow with it.

And as cities grow, attracting more people, increasing the demand for housing our next theme likely will take part in that growth.

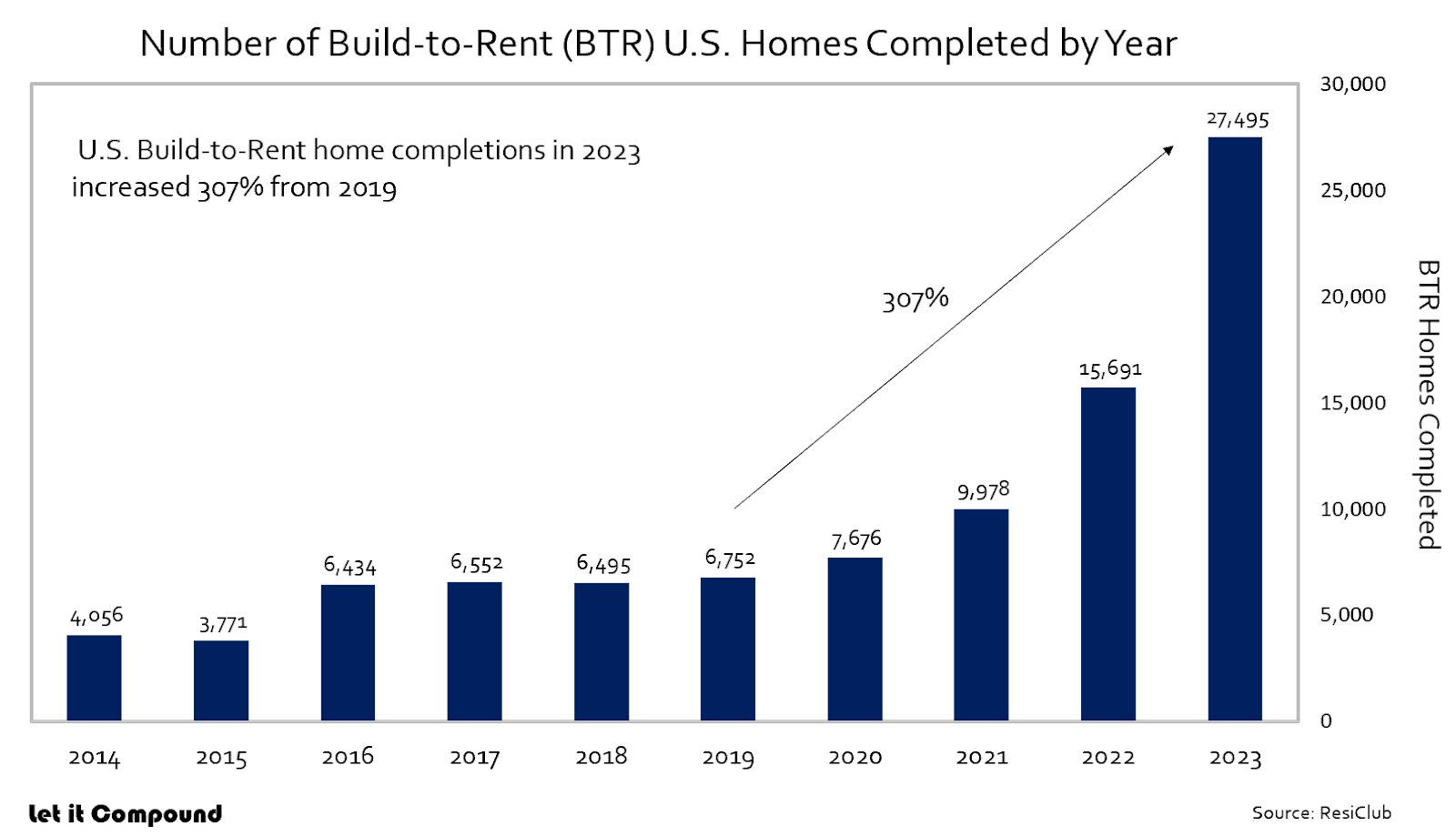

This next theme is Build-to-Rent communities.

Build-to-Rent

Build-to-Rent (BTR) communities are on the rise.

These are single family housing developments generally of 50+ homes built solely for the purpose of renting.

And the community can offer amenities like dog parks, green spaces, community centers, fitness centers, and even pools.

As well, renters get the lifestyle of homeownership without the hassles of maintenance. Many even take care of lawn care - that's appealing.

It's understandable why BTR has taken off.

We can see the growth in the chart below looking at completed BTR single-family homes.

Even with this growth, estimates have BTR units totaling just 350,000 making up just 1.5% of the total single family rental market.

It's an interesting burgeoning opportunity for homebuilders.

These communities have strong financial backing. And are seeking to grow their rental portfolio.

And since the scale of these projects can be sizable making it harder for smaller builders to capitalize on them.

This combination can provide a more stable income stream from these communities as they grow.

It's a positive trend for publicly traded homebuilders.

And our last theme is the state of the economy, it’s humming along.

Things are Pretty Solid

America's economy is growing 2.7% - measured by gross domestic product (GDP). This is nearly 4-times better than JP Morgan's 2024 forecast expecting growth of just 0.7%.

What's more this is while the economies of other major countries like Germany and the United Kingdom, have respective growth rates of 0% and 1.1%.

And per JP Morgan's forecast (to stay consistent with forecasts) the U.S. is expected to expand 2.1% during 2025.

Despite this strong data, a recent survey found 59% of Americans think we are in a recession.

I bring up this point because people are thinking this while:

America is performing better than expected evident in the GDP growth.

Unemployment is at 4.1% below the long-term average of 5.7%.

Inflation is running at 2.9%, down from 9.1% when it recently peaked during the summer of 2022.

Real Wage Growth (wages adjusted for inflation) is at 1%. This is compared to -2.8% the text low in 2022. And have been positive since mid-2023, meaning as a whole people are making more money…

Consumer spending is up 3.7% - biggest increase since the start of 2023.

Construction spending, an indicator of the health of an economy, through the third quarter of 2024 total $1.6 trillion. This is up 7.3% compared to the same period a year prior.

I could go on. However, all these strong data points are occurring while nearly 60% of the country thinks we are in a recession.

People buckle down and spend less during bad times.

So, if these people start feeling good about the economy, we could see strong growth as a country.

In addition, there is improving sentiment amongst homebuilders for a more accommodating regulatory landscape.

To keep it short, there is a lot of red tape when it comes to building homes.

Developments need approvals, inspections, meet certain guidelines of individual municipalities, and so on.

These hurdles are a mix of good and bad.

Like not developing wetlands and destroying important ecosystems - the good.

Bad being overly restrictive zoning hindering the ability to build residential homes.

And with a regime change coming for the U.S. government builders are optimistic in having the ability to develop more lots.

Recently, Carl Harris the Chairman of the NAHB said:

"[Homebuilders are] anticipating future regulatory relief in the aftermath of the election. This is reflected in the fact that future sales expectations have increased to a nearly three-year high.”

All together we have many big themes benefiting homebuilders.

However, I can't not mention what could throw a wrench in this investment thesis.

What Could Tank this Idea

I think it would be disingenuous to only paint a beautiful landscape of happy trees and strong trends for this investment thesis.

The reality is home builders are reliant on a healthy economy, willing banks, and a strong consumer.

And there are three risks that will throw a wrench in this investment thesis:

Recession

Inflation

Elevated interest rates

I understand these may seem obvious because these are risks to essentially all stocks.

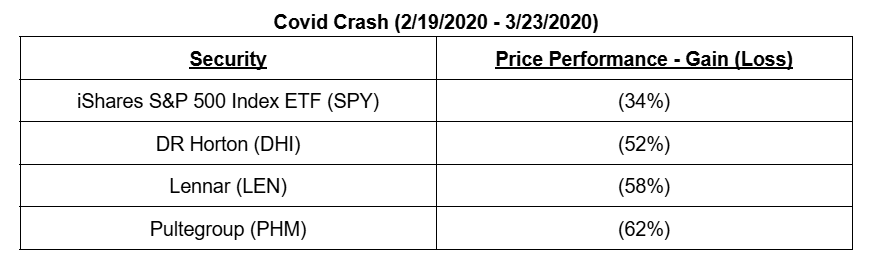

However, homebuilders’ stock prices get whacked during market drawdowns and recessionary periods.

The Covid-19 Crash in early 2020 exemplifies this.

I’m not predicting a recession. Nor am I predicting a market sell-off, though it wouldn't surprise the run up in the S&P 500 over the last two years. The index returned a respective 24.2% and 23.3% for 2023 and 2024.

Next, interest rates staying elevated will keep pressure on affordability. And if housing prices start where they are, or go higher - which I think is likely, builders will have to give concessions to incentivize buyers.

These are incentives like buying down mortgage points I mentioned above. And concessions eat into profit margins.

Unless the companies can offset profit loss with higher growth, their share prices will get whacked.

As for inflation, that's quite the boogeyman as we all have experienced the past couple years.

If we see it come back, we'll likely see equity prices materially fall. We could even see GDP contraction. And the recent inflation data is concerning…

Again, I'm not making any predictions and getting ahead of myself claiming inflation is back. We need more data.

However, if it does come back. To combat inflation interest rates could hike as this is the Fed's playbook. The Fed increasing its Fed Funds rate, not cutting, to again combat inflation is a risk here.

During periods of rate hikes equities have a rough time. In the most recent rate hike cycle where the Fed raised its Fed Funds Rate 525 basis points between March 2022 and July 2023, the S&P 500 fell as much as 18%.

Now for a homebuilder's specific risk - softening demand in select markets.

I'll bring up potential concerning markets, if there are any, for the individual companies.

Right now, though, I'll only mention one market here that's been a frequent question for the executives of homebuilders. And that market is Florida.

During D.R. Horton’s first quarter 2025 earnings call on January 21, 2025, CEO Paul Romanowski. Hei said they have seen:

“Some buildup [in inventory] in the Florida market and certainly in certain of the Florida markets, a little more than others, the same in some of the Texas markets. But across -- generally across the footprint, we feel like inventory is in pretty good shape.”

To move homes excess inventory companies will increase incentives, lowering profit margins.

It makes sense companies upped their Florida presence.

As shown above Florida is experiencing solid pollution growth. Its population has increased by nearly 1.9 million people since 2019.

And along with the population growing so has the number of new homes built in the sunshine state. We'll notice the spike in recent years.

Single Family Homes Built by Year in Florida

Source: University of Florida - Shimberg Center for Housing Studies 2024 Annual Report

Between these new builds and existing homeowners seeking to sell, active listings are around 196K, higher than pre-pandemic levels.

Weakness in Florida could be a canary in the coal mine for other large metros.

Okay - Now What?

Now that we have a jumping off point for homebuilders we can dig into several individual companies.

My goal is to profile companies for future investment.

Currently, I see the top builders as mostly fairly valued. They could go up; however, I wouldn't feel comfortable owning them quite yet.

And recently this cohort of stocks have come down. Which could give us the opportunity to take a starter position in a builder or few.

Builders are giving up margin to move inventory by utilizing incentives.

This will hurt profits in the short run. And that's good for the long-term.

Gaining market share and selling more homes over the long-term is the core of this investment thesis.

I may recommend a name if I find one a bargain while doing more due diligence. Or I'll lay out valuation multiples I'd feel comfortable buying.

Understanding companies, sectors, and having an idea of valuations can allow us to jump on an opportunity if it presents itself.

To be cliche in quoting Buffett “be greedy when others are fearful.”

It's uncomfortable to buy a stock that's falling or has just crashed 30%. All while articles are saying “stay away.”

However, having a backlog of potential investments lets us comfortably buy companies when they go on sale.

And I believe the companies I'll profile are worth owning, just at the right price.

This has been a long one!

I appreciate you reading along.

I may sprinkle in some posts before, or while, profiling our home builders.

Until next time,

Let it Compound.

Disclaimer Time!

As always this is not investment advice. Again, nothing here is investment advice.

This information is for educational and entertainment purposes only.

Please, PLEASE, always do your own due diligence. And if need be, consult with an investment professional regarding your finances.

Amazing deep dive into a sector I did not know but with the structural shortage of housing and market share penetration that you described this might join my watchlist!